Why One Income Is a Liability — And What to Do About It

Most people don’t think about financial risk until something goes wrong. A layoff, a health scare, a company downsizing — and suddenly the paycheck that felt solid for years is just… gone. That single income stream you built your whole budget around disappears, and there’s nothing underneath it.

This isn’t meant to be scary. It’s just an honest way to think about money.

The financial world spends a lot of time telling people to invest better, spend less, save more. All of that matters. But there’s a quieter idea that doesn’t get as much attention: the number of places your money comes from matters just as much as how much of it you have.

The One-Source Problem

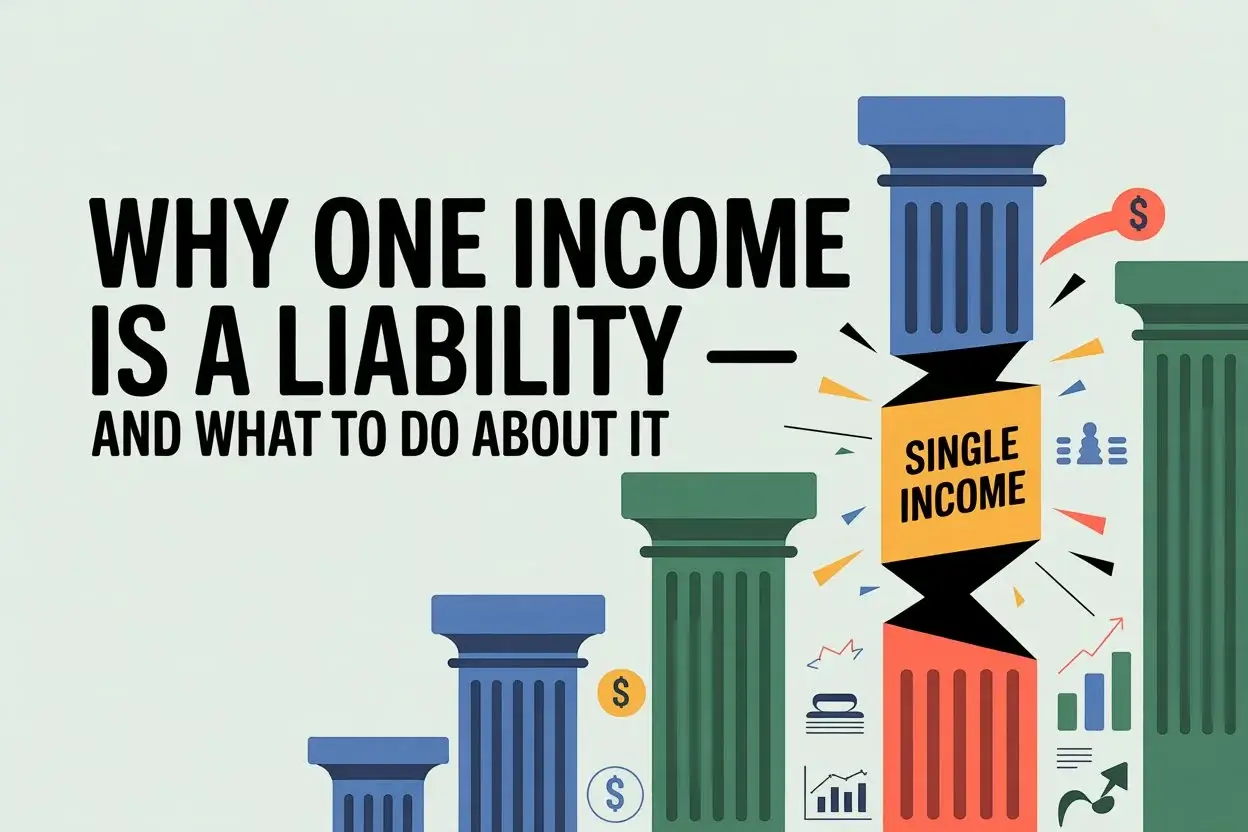

Think of income like a table. If it’s standing on one leg, it tips the moment that leg is compromised. Two legs are more stable. Four legs, and you could lose one entirely and still be fine.

Most working adults have one leg: a job. Some have a side gig. Very few have built income from three or four places — but those who have tend to feel noticeably calmer about money, even if the total amount isn’t dramatic.

That calmness isn’t magic. It’s structural. When one stream slows down, the others are still running.

The goal of building multiple income streams isn’t to get rich overnight. It’s to stop being financially fragile.

What “Multiple Streams” Actually Means

The phrase gets thrown around a lot, usually alongside vague advice about passive income or the promise that you’ll be making money while you sleep. That framing isn’t wrong, but it skips the part where the work happens — and it skips the more important point, which is about stability, not speed.

There are a few broad categories worth understanding:

Active income is money you trade time for. Your job falls here. So does freelancing, consulting, or driving for a rideshare app. It stops when you stop. For those building active income streams through remote freelancing or consulting, digital security is a critical part of your business setup; understanding the different types of VPN can help you protect sensitive client information and secure your financial accounts while working from coworking spaces or public Wi-Fi.

Semi-passive income requires real setup effort up front, then less ongoing work — but it doesn’t fully run itself. Renting a room, selling a digital product you built, or writing a course that still needs occasional updates. The line between “active” and “semi-passive” is blurry, but it’s real.

Passive income is income that genuinely continues without you actively maintaining it. Dividend stocks, index funds in taxable accounts, royalties on work you created years ago. This is the category most people overestimate how quickly they can reach.

The practical reality for most people early in their financial journey is that you can layer all three, just in different proportions depending on your time, energy, and current financial foundation.

Starting Where You Are

Here’s something worth saying plainly: you don’t need to launch a business or invest $50,000 to start diversifying your income. The first step is usually much smaller.

Take someone like Sana, a teacher in her mid-30s. Her primary income is her salary. A few years ago, she started tutoring two students on weekends for a few hours. That’s $400 to $600 a month — not life-changing money, but it’s real income from a second source. When her school’s budget froze and salary raises disappeared for a year, her tutoring kept growing. By the time things normalized at work, she’d built a small but reliable stream that covers her car payment every month without touching her salary.

The scale isn’t the point. The structure is.

What Sana did was reduce the percentage of her income that depended on any one decision she didn’t control.

The Investing Layer

The second category most people can access — even on a modest budget — is investing. This gets treated as something only wealthy people do, but it’s available to almost anyone with a regular income and a little patience.

The mechanics are simple: money in a brokerage account, invested in a diversified index fund, compounds over time and occasionally pays dividends. You’re not picking stocks or timing the market. You’re buying small ownership stakes in hundreds of companies at once, and over the long run, that tends to grow.

The income from this isn’t immediate. You won’t notice it in year one. But at some point — five years, ten years, twenty years in — you’ll have a financial asset that generates returns independent of any employer, client, or customer. That’s a legitimate income stream, even if it starts small.

The key is starting early enough that time does the work. Someone who invests $300 a month starting at 30 ends up in a meaningfully different position at 55 than someone who waits until 40. The math on compounding is real, and most people underestimate it.

Building Something That Earns Without You Being There

This is the part people dream about — income that runs without you actively working for it. And it’s achievable, but it takes honest preparation.

A few paths worth thinking about:

Rental income is one of the oldest wealth-building tools in existence. You don’t need to own multiple properties. Renting out a spare room, a parking space, or a storage area counts. It’s a smaller version of the same principle.

Digital products — things like templates, guides, or recorded courses — can sell repeatedly once built. A photographer who spends a month creating a Lightroom preset pack may earn from that for years. A financial analyst who builds a budgeting spreadsheet template and sells it for $15 might get 200 sales without doing anything after launch. These aren’t huge numbers, but they’re real, and they add up alongside other streams.

Content and royalties take the longest to pay off but have a long tail. A YouTube channel, a book, a podcast with sponsorships — these take years to monetize meaningfully. But people who started three years ago are now earning from content they created once and haven’t touched since.

None of these are shortcuts. They all require work. The difference is that the work is front-loaded rather than ongoing.

The Risk Reduction Angle

Here’s what doesn’t get discussed enough: multiple income streams aren’t just about accumulating more money. They’re about reducing the damage any one event can do to your financial life.

Industries change. Companies restructure. Economic downturns happen with no warning. Someone with three income sources, even modest ones, can usually absorb one disruption without it becoming a crisis. Someone with one source can’t.

This is the same logic behind diversifying an investment portfolio. You don’t put everything in one stock because if that company has a bad year, your entire position suffers. Spreading across sectors and assets means no single failure is catastrophic.

Income works the same way. A person earning $5,000 per month — split between a job, some freelance work, and investment returns — is actually in a more stable position than someone earning $7,000 from a single employer, even though the dollar amount is lower.

Stability has value. Financial anxiety has costs — to health, to decision-making, to relationships. Reducing the risk of income disruption is worth something even if it doesn’t show up directly in your bank balance.

A Note on Sequence

People often want to do everything at once: start a business, invest, freelance, build passive income. That usually leads to doing none of it well.

A more realistic sequence looks like this: stabilize your main income first, then add one secondary stream that’s manageable with your current schedule and budget. Build that until it’s consistent. Then consider adding another.

The order matters. Trying to build passive income before your primary income is secure usually means you’re pulling resources from a situation that needs them. Trying to start a business while carrying high-interest debt often means the business is subsidizing the debt, not building wealth.

Get the foundation stable. Add one stream. Let it mature. Then think about the next one.

What This Looks Like Over Time

Imagine someone at 28 who earns $55,000 a year from their job. They start investing $250 a month into a broad market index fund. By 35, they’ve accumulated enough that dividends and growth add a meaningful return each year — not a second salary, but a real asset.

During those same years, they freelance occasionally in their field. Maybe 10 hours a month. That adds $800 to $1,000 some months, nothing in others.

By the time they’re 40, they have a job that’s grown with their career, an investment portfolio that’s compounding, and a freelance reputation that brings occasional work. Three streams. None of them dramatic. Together, they’ve changed the structure of that person’s financial life.

That’s not a fantasy. That’s a realistic path for someone who makes steady, unglamorous choices over a decade.

Where to Actually Begin

If you’re at the start of this and nothing feels achievable yet, pick one thing.

If you have marketable skills, see if anyone would pay you to use them on a project basis. One client. One engagement. You’ll learn more from that than from any amount of research.

If you have income to invest but don’t know where to start, open a brokerage account, set up automatic contributions to a low-fee index fund, and don’t touch it. Time will do the rest.

If you want to build something more passive, pick the smallest possible version — not a full course, but one useful template. Not a rental property, but a parking space or a room. Start small enough that you can actually finish it.

The goal isn’t to have everything figured out. It’s to stop having only one thing.

Your financial life gets more stable the more sources it has. That stability compounds just like money does — quietly, invisibly, until one day you realize you’ve built something that can actually hold up.