Risk Management in Investing: How to Protect Your Money While Growing Wealth

Here’s something nobody tells you when you start investing:

The money you don’t lose matters just as much as the money you make.

Everyone talks about returns. Which stocks are hot. What’s going to 10x. How to get rich quick.

But successful investors? They’re obsessed with something else: not screwing up.

Markets crash. Companies fail. Economies stumble. Even the smartest investors get blindsided sometimes. That’s just reality.

This is why risk management — learning how to protect your money while still growing it — is one of the most valuable skills you can develop as an investor.

Let’s break down how it actually works.

What Is Risk Management in Investing?

Risk management is basically the process of identifying, understanding, and controlling potential losses in your investment portfolio.

Every investment carries some level of risk:

- Market swings (stocks go up and down)

- Economic downturns (recessions happen)

- Company failures (even big companies can collapse)

- Inflation (your money loses purchasing power over time)

The goal of risk management isn’t to eliminate risk entirely — that’s impossible. Instead, it’s about making sure risks are:

- Controlled and manageable

- Spread out (diversified)

- Aligned with your financial goals and timeline

In simple terms, risk management answers one critical question:

How much risk should you take to reach your goals without exposing yourself to unnecessary losses?

Why Risk Management Actually Matters

A lot of beginners obsess over returns. “I want 20% gains!” “What stock will double?”

But experienced investors know something crucial: avoiding big losses is just as important as making gains.

Here’s why: If your portfolio loses 50%, you need a 100% gain just to break even.

Let that sink in. Lose half, and you need to double just to get back to where you started.

Because of this math, managing downside risk is critical for long-term success.

Good risk management helps you:

- Reduce wild portfolio swings

- Avoid catastrophic losses that set you back years

- Keep your emotions in check during crashes

- Stay invested for the long haul

Bottom line: strong risk management dramatically improves your odds of reaching your financial goals.

The Different Types of Investment Risk

Risk comes in different flavors. Let’s break them down:

Market Risk

This is the risk that the overall market tanks, dragging almost everything down with it.

Think:

- Economic recessions

- Financial crises (like 2008)

- Global events (pandemics, wars, political chaos)

Even diversified portfolios can’t completely escape market risk. When everything’s falling, there’s nowhere to hide.

Company-Specific Risk

This is the risk that a specific company you own blows up.

Maybe:

- Management makes terrible decisions

- Revenue collapses

- A competitor destroys their business model

- Accounting fraud gets exposed

This is why owning individual stocks is riskier than owning index funds. One company can go to zero.

Inflation Risk

Inflation slowly eats away at your money’s purchasing power.

If your investments grow 3% but inflation is 4%, you’re actually losing purchasing power — even though your account balance went up.

This is why keeping everything in cash or bonds long-term is dangerous. You need growth assets like stocks to outpace inflation.

Interest Rate Risk

When interest rates change, certain investments get hit harder:

- Bonds (lose value when rates rise)

- Real estate (harder to finance when rates are high)

- Growth stocks (less attractive when safe bonds pay more)

You can’t control interest rates, but you can understand how they affect your investments.

Liquidity Risk

This is the risk that you can’t sell an investment quickly without taking a huge loss.

Real estate is a classic example. If you need cash fast and the market’s slow, you might have to sell at a terrible price.

Some small stocks also have liquidity issues — nobody’s buying when you want to sell.

Key Principles of Smart Risk Management

Successful investors rely on a few core strategies to manage risk:

1. Diversification (Don’t Put All Your Eggs in One Basket)

Diversification is the most powerful risk management tool that exists.

Instead of betting everything on one stock or one sector, you spread your money across:

- Different stocks

- Different sectors (tech, healthcare, consumer goods)

- Different asset types (stocks, bonds, real estate)

- Different countries (U.S. and international)

Why this works:

If one investment crashes, the others can offset the damage.

For example: Tech stocks tank, but your healthcare and utility stocks hold steady. Your portfolio drops a little instead of getting destroyed.

The easiest way to diversify? Broad market index funds. Instant diversification in one purchase.

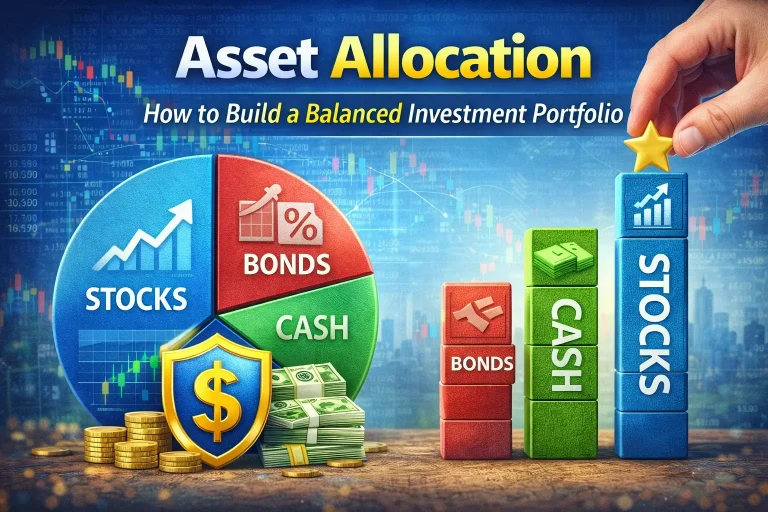

2. Asset Allocation (The Right Mix for Your Situation)

Asset allocation means how you divide your money between different types of investments.

A typical portfolio might look like:

- 60% stocks (for growth)

- 30% bonds (for stability)

- 10% other stuff (real estate, cash, alternatives)

Your allocation should match:

- Your timeline (how long until you need the money)

- Your risk tolerance (can you sleep at night if stocks drop 30%?)

- Your goals (retirement? house down payment? financial independence?)

General rule:

- Younger investors → more stocks (time to recover from crashes)

- Older investors → more bonds (need stability, less time to recover)

3. Position Sizing (Don’t Bet the Farm on One Thing)

Position sizing means limiting how much you put into any single investment.

Common rules:

- Don’t put more than 5–10% of your portfolio in a single stock

- Avoid getting too concentrated in one sector

Why this matters:

If you put 50% of your money in one stock and it crashes, you’re screwed. If you put 5% and it crashes, it’s annoying but survivable.

4. Regular Rebalancing (Stay on Track)

Over time, some investments grow faster than others, throwing off your target allocation.

Example:

- You start with 60% stocks / 40% bonds

- Stocks have a great year and grow to 75% of your portfolio

- Now you’re taking more risk than you planned

Rebalancing means periodically selling some winners and buying some losers to get back to your target.

This forces you to “sell high, buy low” systematically — exactly what you should be doing.

The Hidden Risk: Your Own Brain

Here’s the uncomfortable truth:

One of the biggest risks to your portfolio is YOU.

Investors constantly sabotage themselves through emotional decisions:

- Panic selling during crashes (locking in losses)

- FOMO buying during bubbles (buying high)

- Chasing hot stocks (usually right before they crash)

Behavioral mistakes can destroy your long-term returns faster than any market crash.

How to Protect Yourself from Yourself:

- Automate your investing (removes emotion)

- Build a diversified portfolio and leave it alone

- Have a plan and stick to it (don’t wing it)

- Stop checking your portfolio every day (seriously, it just stresses you out)

Emotional discipline is often the difference between successful and unsuccessful investors.

Advanced Risk Management Strategies

Once you’ve got the basics down, here are some more sophisticated approaches:

Risk-Adjusted Returns

Don’t just look at raw returns. Look at how much risk you took to get those returns.

Two portfolios might both make 8% annually, but if one swings wildly and the other is steady, the steady one is actually better — less stress, more sleep.

Hedging Strategies

Hedging means using financial tools to reduce potential losses.

Examples:

- Options strategies

- Inverse ETFs (go up when the market goes down)

- Diversifying into uncorrelated assets

Fair warning: Hedging adds complexity and costs. Most beginners don’t need it.

Emergency Cash Reserves

This might seem unrelated to investing, but hear me out:

If you have 6–12 months of expenses in cash, you won’t be forced to sell investments during a crash when you need money for an emergency.

A strong financial foundation indirectly protects your investment portfolio by keeping you invested during tough times.

Risk Management for Long-Term Investors

Long-term investors have a huge advantage: time.

Markets crash, but they also recover. Always have, historically.

Long-term risk management focuses on:

- Staying diversified

- Investing consistently (even during crashes)

- Avoiding speculation and gambling

- Keeping your eye on long-term goals

Over long periods, patience becomes your best risk management tool.

Risk Management and Financial Independence

If you’re pursuing financial independence or early retirement, risk management becomes even more critical.

Why? Because a major screwup can delay your goals by years — or even derail them completely.

On the flip side, a well-managed portfolio lets you grow wealth steadily while protecting what you’ve already built.

Most successful FIRE strategies rely on balanced portfolios that manage volatility while still providing growth.

It’s not about getting rich quick. It’s about getting rich reliably.

Final Thoughts: Protection Enables Growth

Risk management isn’t about being scared or overly cautious.

It’s about being smart.

Sure, chasing high returns sounds exciting. But sustainable wealth? That’s built through balanced strategies that carefully manage risk.

The essentials:

✅ Diversify (spread your bets)

✅ Use smart asset allocation (right mix for your situation)

✅ Control your emotions (don’t panic, don’t get greedy)

✅ Think long-term (patience beats cleverness)

By doing these things consistently, you create a portfolio capable of growing wealth while surviving market chaos.

Remember: the goal of risk management is simple:

Protect your capital so it can keep compounding for decades.

Do that, and you’ll be ahead of 90% of investors out there.