FIRE Strategies: Your Complete Guide to Reaching Financial Independence

Here’s something most people get wrong about FIRE:

They think it’s a single, rigid formula. Save 70% of your income, live on rice and beans, retire at 35.

That’s not what FIRE is.

FIRE is a framework — and within that framework, there are multiple paths you can take depending on what kind of life you’re actually trying to build.

Some people want to escape work as fast as humanly possible. Others want flexibility without fully retiring. Some want to maintain luxury. Others find freedom in simplicity.

The “right” FIRE strategy completely depends on your goals, income, personality, and what you’re willing to sacrifice.

In this guide, we’ll walk through the most common FIRE strategies, how they actually work, who they’re best for, and how to figure out which one fits your life.

The Foundation Every FIRE Strategy Shares

Before we dive into specific approaches, let’s establish the core principle:

Financial Independence = Your investments generate enough income to cover your annual expenses

Most FIRE strategies use the 4% rule, which came from the Trinity Study analyzing historical market returns.

The simplified formula:

Portfolio Needed = Annual Expenses × 25

Quick example:

If you spend $60,000 per year

You need approximately $1.5 million invested.

Every FIRE strategy essentially modifies one of two variables:

- Your annual expenses (spend less)

- Your income and savings rate (earn and save more)

Everything else is just optimization around those two levers.

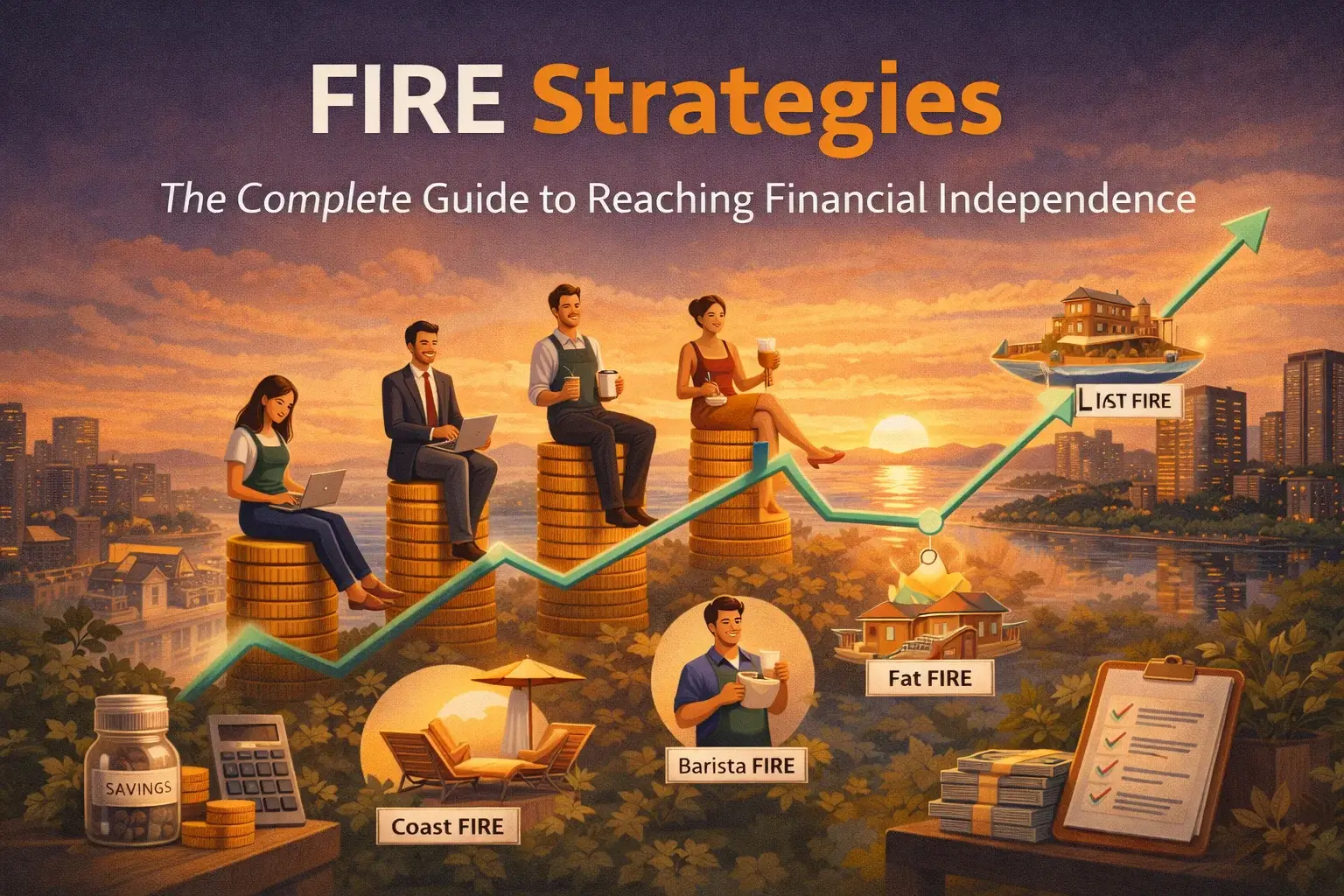

The 7 Main FIRE Strategies (and Who They’re For)

Let’s break down the most common paths people take.

1. Lean FIRE

The idea: Retire early by living on a minimalist budget

Portfolio target: $750k–$1.5M typically

Timeline: Fastest route to freedom

Lean FIRE is all about cutting expenses to the bone and reaching independence as quickly as possible.

You typically:

- Keep housing costs very low (small home, roommates, or LCOL area)

- Avoid lifestyle inflation like the plague

- Maintain a very high savings rate (50–70%)

- Live intentionally on $30k–$50k per year

Best for:

- Minimalists who genuinely enjoy simple living

- Digital nomads

- People who value time and freedom over consumption

- Those willing to be very disciplined with spending

The tradeoff: Less financial cushion for unexpected expenses. Market downturns are scarier.

2. Fat FIRE

The idea: Achieve financial independence while maintaining (or upgrading) your lifestyle

Portfolio target: $2M–$5M+

Timeline: Longer accumulation phase

Fat FIRE is for people who want freedom without cutting back on the good life.

You typically:

- Maintain comfortable spending ($80k–$150k+ per year)

- Build multi-million-dollar portfolios over 15–25 years

- Focus heavily on tax optimization and estate planning

- Keep working high-income jobs longer

Best for:

- High earners (executives, doctors, tech workers, entrepreneurs)

- People who genuinely enjoy their lifestyle and don’t want to downgrade

- Those with strong earning power willing to work longer for comfort

The tradeoff: Requires significantly more capital and usually means more years in demanding careers.

3. Barista FIRE

The idea: Reach partial financial independence and supplement with chill part-time work

Portfolio target: Moderate (often $800k–$1.2M)

Timeline: Medium (faster than full FIRE, slower than Lean FIRE)

Barista FIRE lets you quit the corporate grind without fully retiring.

You typically:

- Leave stressful full-time work

- Pick up flexible, low-stress part-time work (20–30 hours/week)

- Use investments to cover most expenses

- Work primarily for health insurance and supplemental income

Best for:

- Burned-out professionals who want out of corporate life

- People who enjoy working but not 50+ hours a week

- Those who need employer health insurance (big in the U.S.)

- Anyone seeking flexibility over full retirement

The tradeoff: You’re still working and relying on earned income. Not true full independence.

4. Coast FIRE

The idea: Front-load your investing, then “coast” to traditional retirement

Portfolio target: Smaller early on, grows passively over time

Timeline: Aggressive saving early, then relaxed later

Coast FIRE means you invest heavily in your 20s and 30s, then stop contributing entirely and let compound growth do the rest.

You typically:

- Aggressively save early in your career

- Once your portfolio is large enough to grow into full retirement by age 60–65, you stop saving

- Work just enough to cover current expenses (no more 401k contributions)

- Let your investments compound untouched

Best for:

- Younger professionals who start investing early

- People who want lower financial pressure later in life

- Those who enjoy their work but want less savings stress

The tradeoff: You’re still working full-time for years. You’re not withdrawing or retiring early — you’re just reducing the pressure.

5. Slow FIRE

The idea: Save consistently but moderately, retire closer to traditional age

Portfolio target: Similar to conventional retirement

Timeline: Extended (retire at 50–60 instead of 30–40)

Slow FIRE is basically “traditional retirement, but done intentionally.”

You typically:

- Save 15–30% consistently

- Avoid extreme frugality or lifestyle sacrifice

- Accept a longer timeline to financial independence

- Balance enjoying life now with saving for later

Best for:

- People who genuinely enjoy their careers

- Those unwilling to make major lifestyle sacrifices

- Folks who want security without pressure

The tradeoff: Freedom comes later. You’re working well into your 50s.

6. Geographic Arbitrage FIRE

The idea: Lower your cost of living to dramatically reduce your FIRE number

Portfolio target: Smaller due to reduced expenses

This strategy involves earning money in a high-income country (like the U.S.) and retiring somewhere with a much lower cost of living (like Portugal, Mexico, Thailand, or rural U.S.).

You typically:

- Earn in dollars, euros, or pounds

- Retire somewhere expenses are 50–70% lower

- Reduce your annual spending from $70k to $35k just by relocating

Best for:

- Remote workers and digital nomads

- Expats comfortable living abroad

- Flexible people open to cultural adjustment

The tradeoff: Cultural and logistical challenges. Distance from family. Different healthcare systems.

7. Entrepreneurial FIRE

The idea: Build and sell a business instead of relying purely on salary savings

Portfolio target: Varies wildly

Instead of slowly saving salary over 20 years, this path involves building a business, scaling it, and selling for a lump sum.

You typically:

- Build a business with real equity value

- Scale revenue over 5–10 years

- Sell the company or take it public

- Use the liquidity event to instantly hit your FIRE number

Best for:

- Risk-tolerant founders and builders

- People with entrepreneurial skills

- Those willing to bet on themselves

The tradeoff: High volatility, uncertainty, and failure risk. Most businesses don’t result in big exits.

The 4 Strategic Levers That Control Every FIRE Plan

No matter which strategy you choose, your path to FIRE boils down to these four levers:

1. Income Expansion

Increasing your income is the fastest way to shorten your timeline.

Examples:

- Negotiating raises aggressively

- Switching to higher-paying industries (tech, finance, healthcare)

- Building side businesses

- Acquiring equity compensation

A $50k salary increase can cut 5+ years off your timeline.

2. Savings Rate Optimization

Your savings rate matters more than investment returns in the early years.

A 20% savings rate vs. a 50% savings rate can literally be the difference between retiring at 60 vs. 45.

Even small increases compound massively over time.

3. Investment Efficiency

Most FIRE strategies rely on:

- Broad index funds (S&P 500, total market)

- Tax-advantaged accounts (401(k), IRA, HSA)

- Taxable brokerage accounts for early retirement access

- Real estate (optional, some people love it)

At higher net worth levels, tax strategy becomes as important as returns. Smart tax planning can save you hundreds of thousands.

4. Expense Design

This isn’t just about spending less — it’s about intentional lifestyle design.

Lower fixed costs mean:

- Smaller/cheaper housing

- Modest or no car payments

- Minimal recurring subscriptions

Your fixed expenses determine how much freedom you need to buy. The lower they are, the less you need saved.

How to Choose the Right FIRE Strategy for You

Ask yourself these questions:

- Do I want to stop working completely, or just work on my terms?

- Am I willing to significantly reduce my lifestyle?

- How much income potential do I realistically have?

- Do I genuinely enjoy my work, or do I want out ASAP?

- How much risk and uncertainty can I handle?

If you want speed → Lean FIRE

If you want comfort → Fat FIRE

If you want flexibility → Barista FIRE

If you want early security but not early retirement → Coast FIRE

If you want to relocate → Geographic Arbitrage

If you’re entrepreneurial → Build and sell a business

The best strategy isn’t the one with the best math — it’s the one that aligns with your personality and values.

Risk Management No Matter Which Strategy You Choose

Regardless of which path you take, you need to think about:

- Sequence of returns risk (retiring right before a crash)

- Inflation eating away purchasing power

- Healthcare costs before Medicare (U.S.-specific nightmare)

- Tax drag on withdrawals

- Lifestyle inflation creeping up over time

Many experienced FIRE planners use:

- 3–3.5% withdrawal rates (more conservative than 4%)

- Cash buffers of 1–3 years expenses

- Diversified portfolios across asset classes

- Flexible spending strategies during downturns

Early retirement means your portfolio needs to last 40–50 years, not 25–30.

That changes everything.

Is There a “Best” FIRE Strategy?

No.

The best FIRE strategy is the one you can actually execute consistently for 10–20 years.

Aggressive strategies fail when people burn out.

Ultra-frugal plans fail when the lifestyle becomes unbearable.

High-income plans fail if your career stalls or you hate your job.

Sustainability matters more than intensity.

A Practical Starting Framework

If you’re not sure where to begin, here’s a simple process:

- Track your annual expenses for 2–3 months

- Calculate your baseline FIRE number (Expenses × 25)

- Evaluate your income growth potential realistically

- Decide which lifestyle tradeoffs you’re willing to make

- Choose a strategy that fits your personality

- Commit and adjust as you go

Clarity eliminates confusion. Once you have a clear strategy, execution becomes way easier.

Final Thoughts: FIRE Is a Strategy, Not a Dogma

FIRE isn’t about extreme frugality or extreme wealth.

It’s about intentional financial design.

Some people pursue Lean FIRE because they value time over stuff.

Some pursue Fat FIRE because they’ve worked hard and want comfort.

Some choose Barista or Coast FIRE because they want balance and flexibility.

There’s no universal “right” path.

There’s only the strategy that fits your life goals, risk tolerance, income potential, and what genuinely makes you happy.

When you understand the different FIRE strategies clearly, financial independence stops being a vague internet trend, and becomes a concrete, actionable plan you can actually execute.