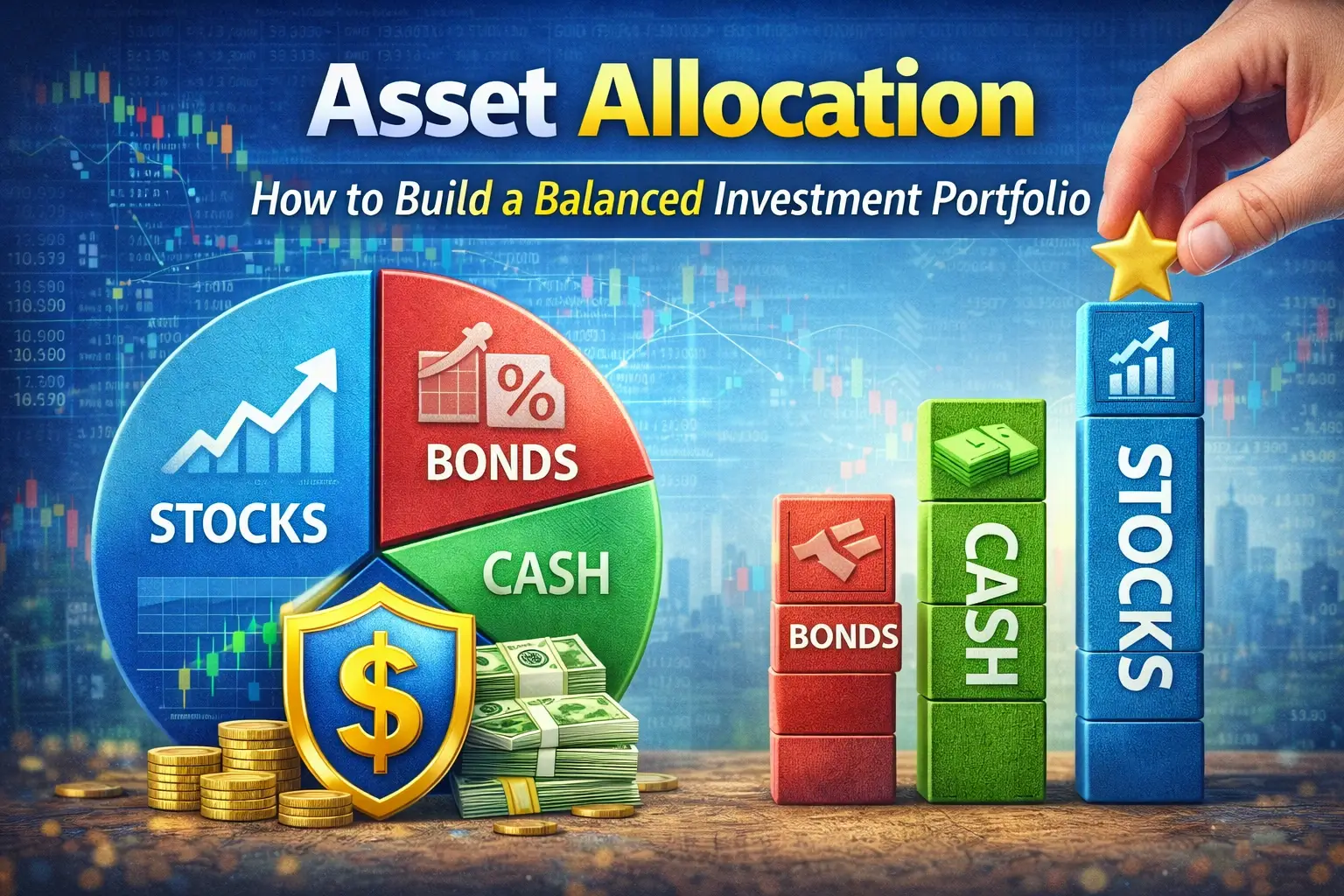

Asset Allocation How to Build a Balanced Investment Portfolio

Here’s something that might surprise you:

Picking the “perfect stock” matters way less than you think.

Most beginners obsess over finding the next Apple or Amazon. They spend hours researching individual companies, reading stock tips, watching YouTube videos about hot picks.

Meanwhile, experienced investors are focused on something completely different: how they divide their money between different types of investments.

This is called asset allocation, and research consistently shows it matters far more than which specific stocks you pick.

A smart asset allocation strategy helps you balance risk, improve diversification, and actually reach your long-term financial goals — without losing sleep over market swings.

Let’s break down what it is and how to do it right.

What Is Asset Allocation?

Asset allocation is simply how you divide your investment money among different types of assets.

The main types are:

- Stocks (equities — ownership in companies)

- Bonds (fixed income — loans to governments or companies)

- Cash (savings accounts, money market funds)

- Alternative assets (real estate, commodities, etc.)

Each type behaves differently during various market conditions. By combining them smartly, you can reduce overall risk while maintaining growth potential.

In simple terms, asset allocation answers one question:

How much of your money should go into each type of investment?

Why Does Asset Allocation Matter So Much?

Asset allocation is the foundation of your investment strategy because it directly affects:

- Your portfolio’s risk level

- Your potential returns

- How stable things are during crashes

- Your long-term outcomes

Example:

A portfolio with 100% stocks might offer higher growth potential, but it’ll also swing wildly and potentially tank 50% during a recession.

A portfolio with 100% bonds might be super stable, but it’ll grow slowly and might not even beat inflation.

The goal? Find the right balance between growth and stability for your situation.

Understanding the Main Asset Classes

Let’s break down the building blocks:

Stocks (Equities)

Stocks represent ownership in companies and are typically the growth engine of your portfolio.

What they offer:

- Higher long-term return potential

- Exposure to economic growth

- Dividend income from some companies

The catch:

- They can swing wildly in the short term

- You might lose 30–50% during crashes

Bonds (Fixed Income)

Bonds are basically loans you make to governments or corporations in exchange for interest payments.

What they offer:

- More stable, predictable returns

- Lower volatility than stocks

- Regular income payments

Why people use them:

- To reduce overall portfolio risk

- To balance out stock volatility

- To preserve capital as they get closer to retirement

Cash and Cash Equivalents

This includes:

- Savings accounts

- Money market funds

- Short-term treasury bills

What cash provides:

- Instant liquidity (can access it anytime)

- Complete stability (no market risk)

- Protection during crashes

The downside:

- Lowest long-term returns (often barely beats inflation)

- Money loses purchasing power over time

Alternative Assets

Some investors add things like:

- Real estate

- Commodities (gold, oil)

- Infrastructure funds

These can behave differently from stocks and bonds, which adds another layer of diversification.

What Determines Your Asset Allocation?

There’s no one-size-fits-all portfolio. Your allocation depends on several personal factors:

1. Your Time Horizon (How Long Until You Need the Money)

Long time horizon (20+ years):

You can handle more stocks because you have time to ride out crashes and recoveries.

Short time horizon (1–5 years):

You need more stability, so increase bonds and cash to reduce volatility.

Example:

A 25-year-old saving for retirement? Go heavy on stocks.

A 60-year-old retiring in 3 years? Shift toward bonds and cash.

2. Your Risk Tolerance (How You Handle Volatility)

Some people can watch their portfolio drop 30% and sleep fine. Others panic and sell everything.

Be honest with yourself:

- Can you stomach big swings?

- Will you panic-sell during crashes?

- Do you check your portfolio constantly and stress out?

Your risk tolerance helps determine how much stock vs. bond allocation makes sense for you.

3. Your Financial Goals

Different goals need different strategies:

- Retirement savings → long-term growth focus

- House down payment in 3 years → stability focus

- Building passive income → dividend and income focus

- Preserving wealth → conservative, low-risk focus

Your portfolio should match what you’re actually trying to accomplish.

Common Asset Allocation Models

Here are some typical portfolio structures:

Conservative Portfolio (Safety First)

Example allocation:

- 30% stocks

- 50% bonds

- 20% cash

Who it’s for:

- People close to retirement

- Low risk tolerance

- Need stability over growth

Balanced Portfolio (Middle Ground)

Example allocation:

- 60% stocks

- 30% bonds

- 10% cash

Who it’s for:

- Most people in their 40s–50s

- Moderate risk tolerance

- Want growth with some stability

Growth Portfolio (Maximum Long-Term Growth)

Example allocation:

- 80–90% stocks

- 10–20% bonds

Who it’s for:

- Younger investors (20s–30s)

- Long time horizon

- High risk tolerance

- Pursuing financial independence

Strategic vs. Tactical Asset Allocation

There are two main approaches:

Strategic Asset Allocation (The Simple Way)

Set it and (mostly) forget it.

You pick a long-term target allocation and stick with it, rebalancing periodically to maintain it.

Example: 70/30 stocks/bonds, rebalance once a year.

This approach focuses on discipline and long-term planning rather than trying to time the market.

Tactical Asset Allocation (The Active Way)

Adjust based on market conditions.

You temporarily shift allocations based on what you think will happen:

- Increase stocks when you think the economy will grow

- Increase bonds when you think a recession is coming

The problem? This requires a lot of knowledge, experience, and time. Most people aren’t good at it.

For most investors, strategic allocation is the smarter choice.

Diversification Within Asset Classes

Asset allocation isn’t just about stocks vs. bonds. You also need diversification within each asset class.

For stocks, diversify across:

- Different industries (tech, healthcare, energy)

- Company sizes (large-cap, small-cap)

- Geographic regions (U.S. and international)

Why? If one sector crashes, the others can help cushion the blow.

The easiest way to achieve this? Broad market index funds. Instant diversification in one purchase.

Rebalancing Your Portfolio (Stay on Track)

Over time, your allocation drifts away from your target.

Example:

You start with 70% stocks / 30% bonds.

Stocks have a great year and grow to 85% of your portfolio.

Now you’re taking more risk than you planned.

Rebalancing means selling some of what’s grown and buying what hasn’t to get back to your target.

Common approaches:

- Calendar-based: Rebalance once a year

- Threshold-based: Rebalance when allocation drifts 5%+

Rebalancing forces you to “sell high, buy low” systematically — exactly what you should be doing.

The Behavioral Challenge (Don’t Be Your Own Worst Enemy)

One of the hardest parts of asset allocation? Sticking with it during crazy markets.

Common mistakes people make:

- Taking too much risk during bull markets (everything’s going up!)

- Panic-selling during crashes (get me out!)

- Chasing whatever’s hot (FOMO investing)

A disciplined allocation strategy helps you avoid these emotional traps.

Successful investors understand that consistency and patience beat reactive decision-making every time.

Asset Allocation and Long-Term Wealth Building

Over decades, asset allocation plays a massive role in your investment outcomes.

A well-balanced portfolio can:

- Smooth out market volatility

- Improve long-term returns

- Reduce emotional decision-making

- Provide sustainable growth you can actually stick with

Rather than trying to predict short-term movements, smart investors maintain a consistent allocation aligned with their goals and let time do the work.

Final Thoughts: The Foundation of Smart Investing

Asset allocation isn’t sexy or exciting.

You won’t have stories about picking the next Tesla or timing a market crash perfectly.

But here’s what you will have: a portfolio that actually works over the long term.

The key principles are simple:

✅ Diversify across multiple asset types

✅ Match your allocation to your timeline and risk tolerance

✅ Rebalance periodically to stay on track

✅ Stay disciplined during market ups and downs

Asset allocation is one of the most powerful tools you have for managing risk and building wealth.

Get this right, and everything else becomes easier.

Get it wrong, and you’ll either take too much risk (and panic-sell during crashes) or too little risk (and never reach your goals).

So take some time to think through your situation, choose an allocation that makes sense for you, and stick with it.

Your future self will thank you.